Mixture model: several different distributions mixed with different weights.

\[\begin{aligned}

Z &\sim \text{Mult}(\pi_1, \ldots, \pi_K) \\

Y | Z &\sim \mathcal{D}_Z = f_Z

\end{aligned}\]

Very common to use Gaussians for \(\mathcal{D}_k\) but this isn’t necessary.

Mixture Models and Clustering

Mixture models are common for model-based clustering (a parametric alternative to e.g. \(k\)-means).

This is:

Good! A mixture model is predictive, might explain the data, and can be checked with e.g. cross-validation.

Bad! Highly sensitive to specification of distributions.

E-M Algorithm

Iterative optimization algorithm which alternates between computing the expected log-likelihood given parameter guesses (E-Step) and maximizing that expected log-likelihood to update parameter values (M-Step).

Can directly compute E-Step and M-Step outcomes with Gaussian mixtures.

Otherwise, can use numerical optimization for M-Step and Monte Carlo/other methods for E-Step.

What Don’t Mixture Models Tell Us

Mixture models are useful for clustering or generating bimodel distributions. But they are limited for understanding intertemporal dynamics.

For example: we don’t see the persistence of wet/dry states, with frequent switches between them. Is this reasonable?

To address this, we’ll need a generative model for state switching: a Hidden Markov Model.

Markov Chains

Hidden Markov Models

Instead, we might want to model the process that gives rise to a mixture distribution.

One way to do this for time series is with a Hidden Markov Model where the generative model at time \(t\) probability model “switches” probabilistically based on a Markov chain.

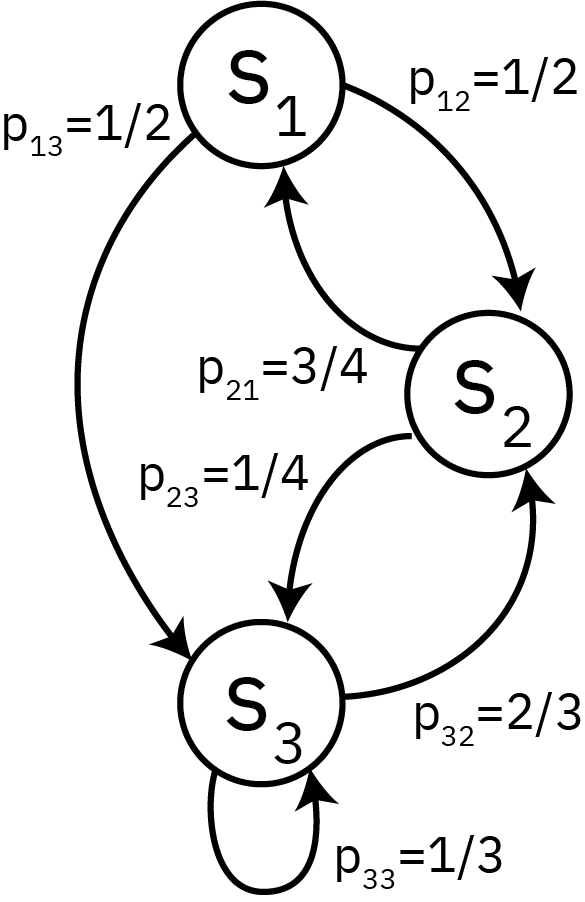

What Is A Markov Chain?

Consider a stochastic process \(\{X_t\}_{t \in \mathcal{T}}\), where

\(X_t \in \mathcal{S}\) is the state at time \(t\), and

\(\mathcal{T}\) is a time-index set (can be discrete or continuous)

\(\mathbb{P}(s_i \to s_j) = p_{ij}\).

Markov State Space

Markovian Property

This stochastic process is a Markov chain if it satisfies the Markovian (or memoryless) property: \[\begin{align*}

\mathbb{P}(X_{T+1} = s_i &| X_1=x_1, \ldots, X_T=x_T) = \\ &\qquad\mathbb{P}(X_{T+1} = s_i| X_T=x_T)

\end{align*}

\]

Example: “Drunkard’s Walk”

:img Random Walk, 80%

How can we model the unconditional probability \(\mathbb{P}(X_T = s_i)\)?

How about the conditional probability \(\mathbb{P}(X_T = s_i | X_{T-1} = x_{T-1})\)?

Example: Weather

Suppose the weather can be foggy, sunny, or rainy.

Based on past experience, we know that:

There are never two sunny days in a row;

Even chance of two foggy or two rainy days in a row;

A sunny day occurs 1/4 of the time after a foggy or rainy day.

Aside: Higher Order Markov Chains

Suppose that today’s weather depends on the prior two days.

Can we write this as a Markov chain?

What are the states?

Weather Transition Matrix

We can summarize these probabilities in a transition matrix\(P\): \[

P =

\begin{array}{cc}

\begin{array}{ccc}

\phantom{i}\color{red}{F}\phantom{i} & \phantom{i}\color{red}{S}\phantom{i} & \phantom{i}\color{red}{R}\phantom{i}

\end{array}

\\

\begin{pmatrix}

1/2 & 1/4 & 1/4 \\

1/2 & 0 & 1/2 \\

1/4 & 1/4 & 1/2

\end{pmatrix}

&

\begin{array}{ccc}

\color{red}F \\ \color{red}S \\ \color{red}R

\end{array}

\end{array}

\]

Rows are the current state, columns are the next step, so \(\sum_i p_{ij} = 1\).

Weather Example: State Probabilities

Denote by \(\lambda^t\) a probability distribution over the states at time \(t\).